Looking to 2026 for Medical Manufacturing

The Year MedTech Stops Winning Approvals and Starts Winning Scale

2026 is shaping up as a year where the most important advantages in MedTech get less glamorous and more decisive. Many of the categories that dominated headlines over the last two years have crossed the regulatory threshold. That is the moment the narrative changes.

When everyone has an FDA-approved platform, technology does not disappear as a differentiator, but it becomes less explanatory. What starts to matter more is whether a company can industrialize adoption: training capacity, workflow fit, reliability at volume, supply consistency, and the ability to make the experience feel routine, not heroic.

This is the year where the best tech does not automatically win. The best operating system often does.

2026 MedTech Trends to Watch

Below are four trends we think define 2026 and the matchups inside each one.

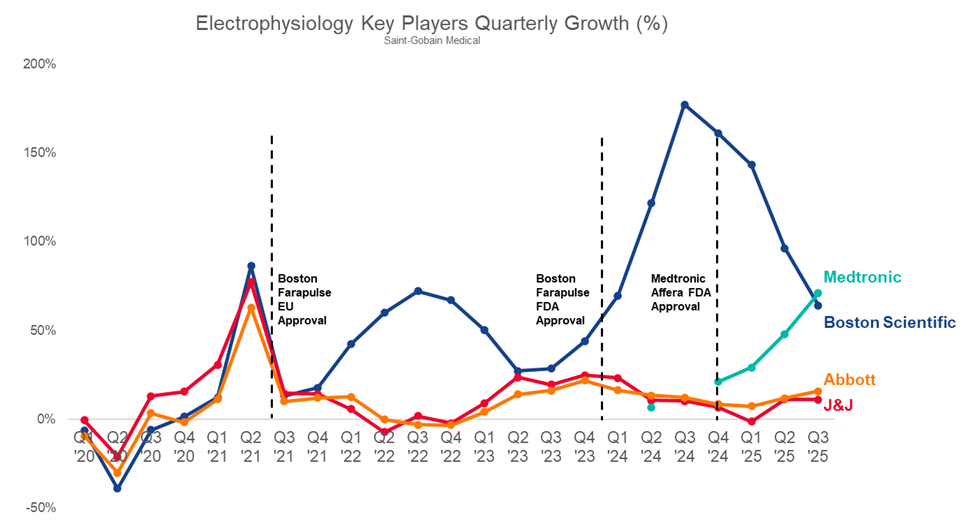

- Pulsed Field Ablation (PFA)

The race moves from waveforms to workflows

- Robotics

Hugo vs Intuitive is a network fight, not a spec sheet fight

- Renal Denervation

Reimbursement opens the door, but workflow decides the pace

- Spin-offs

Focus is not a strategy, it is a stress test

PFA: The race moves from waveforms to workflows

Pulsed field ablation (PFA) enters 2026 as a real competitive market. The cast is now complete:

- Boston Scientific has an installed base with FARAPULSE™ PFA and the advantage of being early enough that the category’s muscle memory is being built on its workflow.

- Medtronic has the PulseSelect™ Pulse Field Ablation System and the Affera™ Mapping and Ablation System in the wings, which gives it an interesting “platform breadth” story rather than a single catheter story.

- Johnson & Johnson has the VARIPULSE™ Platform and deep EP ecosystem reach, which matters because Electrophysiology (EP) labs buy systems, not just tools.

- Abbott arrives later with Volt™ PFA System, which makes 2026 the first year we see if a late entrant can win meaningful share by making adoption feel easier, cleaner, and more repeatable than what the market already knows.

Here is the falsifiable call: 2026 PFA share will be decided less by incremental claims about lesion characteristics and more by training throughput and workflow standardization.

The reason is simple. PFA is no longer fighting for belief. It is fighting for habit. In EP, the product that wins is often the one that makes the lab feel calmer on a busy day. That is not poetry. That is purchasing reality.

Once platforms are approved, the risks become operational and self-inflicted: variable results outside centers of excellence, bottlenecks in proctoring and training, supply constraints, or small workflow frictions that compound.

Abbott’s late entry with Volt is the most interesting strategic test in 2026 as it can be an advantage if the market is still early enough that workflow is malleable and switching costs are not yet cemented. Abbott does not need to convince anyone that PFA works, it needs to convince them that its solution is the path of least resistance to scaling a program.

What we’re watching in 2026

- Training and proctoring capacity, because it controls adoption velocity more than marketing ever will

- Mapping and workflow integration choices that reduce setup time and variability

- Community-hospital performance and early reputation formation, because perception hardens fast in EP

- Any supply tightness, because nothing stalls a category like “we can’t get the catheters”

Robotics: Medtronic Hugo™ RAS System vs Intuitive Surgical

A network fight, not a spec sheet fight

Medtronic’s Hugo finally becoming a US story is one of the few moments in recent robotics where the conversation can shift from “challengers exist” to “challengers can build a footprint.”

Intuitive has a two-decade head start, but it is not primarily a technology head start. It is a system head start: installed base, service infrastructure, training pipelines, credentialing norms, instrumentation economics, and an ecosystem that makes da Vinci feel like default.

Hugo’s 2026 question is not “Is it good?” The question is if Medtronic will build a program that hospitals trust enough to normalize.

Here is the falsifiable call: Hugo’s near-term battleground will be uptime, instrument availability, and service response times in real-world sites, not surgeon preference in flagship centers.

Robotic surgery adoption is a confidence game. A hospital will forgive a learning curve, it will not forgive downtime and supply friction. Utilization is the only metric that matters long-term, and utilization is what breaks when the operational scaffolding is not there.

Medtronic does have a strategic lever Intuitive cannot fully replicate: breadth across the operating room (OR) ecosystem. If Medtronic can package robotics into a broader “surgical operating system” story, it can change procurement dynamics. But that only works if the robot behaves like infrastructure, not like a pilot project.

What we’re watching in 2026

- Evidence of repeatable utilization beyond early adopter sites

- Signals around service model quality and uptime

- Instrument and consumable economics that influence case adoption

- Any meaningful expansion beyond the initial wedge, because that is how programs become platforms

Renal Denervation

Reimbursement opens the door, but workflow decides the pace

Renal denervation is one of those categories that always looked like it should work commercially and then repeatedly struggled to become routine. That story changes only when reimbursement becomes real and operational pathways become buildable.

The current competitive set is anchored by Medtronic’s Symplicity Spyral and Recor’s Paradise. Both are now in the market, and Centers for Medicare & Medicaid Services ( CMS) coverage under Coverage with Evidence Development (CED) creates a structured path to adoption.

Here is the falsifiable call: 2026 renal denervation growth will be gated more by patient identification, referral pathways, and follow-up infrastructure than by debates about energy modality.

Hypertension is everyone’s patient and therefore no one’s procedure. That is the core commercialization problem. Unlike EP or structural heart, there is not a natural procedural culture with established referral mechanics. The product is not just a catheter. The product is a program.

Boston Scientific is the “timeline watch” subplot: how quickly can they move from program to product in renal denervation? The move to acquire SoniVie signals intent and a belief that this category is finally becoming real. 2026 will tell us how quickly a major commercial machine can translate strategic positioning into a credible timeline.

What we’re watching in 2026

- How quickly sites can operationalize evidence workflows under CED

- The emergence of repeatable referral channels beyond specialists already convinced

- Who builds the most scalable “program kit” around patient selection and follow-up

- Whether adoption concentrates in a small number of centers or spreads into broader health systems

MedTech Spin-offs

Focus is not a strategy, it is a stress test

Spin-offs always arrive wrapped in the same promise: focus unlocks performance. Sometimes that is true, but the first year is less about strategy and more about execution under a microscope.

Johnson & Johnson’s planned Orthopedics separation and Medtronic’s Diabetes separation put 2026 in the window where the real work happens: standing up standalone operations, retaining key talent, resetting cost structures, and proving that the newly focused entity can move faster without losing reliability.

Here is the falsifiable call: in 2026, the biggest determinant of spin-off success will be whether product and operational execution improves during the transition, not after it.

The bear case for spin-offs is not that focus is a lie, it is that separation creates drag. Shared services become visible costs. Teams get distracted. Decision-making slows before it speeds up. Competitors take advantage of the fog.

The bull case is that these businesses stop being “one of many” and become the full story, which forces sharper portfolio choices and faster iteration. Diabetes, in particular, is a market where focus can pay off quickly because competition is relentless and expectations are increasingly consumer-grade.

But there is no free lunch. A spin-off is an accountability machine. It makes strengths clearer, and it also makes weak spots impossible to hide.

What we’re watching in 2026

- Talent retention in engineering and field teams, because that predicts execution more than any slide does

- Evidence that R&D decisions are getting sharper, not just cheaper

- Supplier and quality stability during transition, because separation is when problems surface

- Whether the standalone narrative becomes more specific and coherent over time, not more generic

The 2026 Takeaway: Winners Make Adoption Feel Routine

If 2024 and 2025 were about proving categories, 2026 is about scaling them.

- PFA becomes a workflow and training contest.

- Hugo becomes a reliability and utilization contest against a two-decade network.

- Renal denervation becomes a reimbursement-plus-program contest.

- Spin-offs become an execution-under-pressure contest.

The unifying theme is operational scale. That is what creates durable advantage once approvals are no longer scarce.

One last falsifiable call to end on: by the end of 2026, the companies viewed as “leading” in these categories will be the ones that made adoption feel boringly repeatable, not the ones that had the most exciting deck.

FARAPULSE™ is a trademark of Boston Scientific.

PulseSelect™, Affera™ and Hugo™ are trademarks of Medtronic.

VARIPULSE™ is a trademark of Johnson & Johnson

Volt™ is a trademark of Abbott

Da Vinci® is a trademark of Intuitive Surgical.

Key trends reshaped expectations for materials, fluid paths, and manufacturability.

Discover PharmaPure® and PharMed BPT® tubing